Markets were having their best day of 2022. Then Jerome Powell happened. What did the Fed Chair say that had investors concerned?

The first thing we need to understand is that we have been operating in a bearish environment this year. That sets up for bear market-type moves.

For instance, we saw the markets on Monday rebound from a 4%+ down day to close in the green. The only time that has happened is in 2000, 2007, 2008, and 2022. These occurrences were during the internet bubble, crash, the Great Financial Crash, and this year- Bear market-type moves.

Markets rallied 2% ahead of the Fed statement and Powell press conference. However, that was likely shorts covering ahead of the risk event rather than meaningful buying.

Such moves are ripe for reversal. When Jerome Powell failed to appease doves and held steadfast with his hawkish commentary, weak handed longs that took part in the rally headed for the exit.

The reality is that Jerome Powell did not change the narrative. His comments were in line with what we saw at the December 15 Fed meeting and his January 11 nomination hearing. He did expand upon comments on the balance sheet that likely rattled some feathers.

Some of the highlights from the call:

-

- Fed Chair Powell said that he did not believe asset prices themselves represent a significant threat to financial stability since households and businesses are in good shape financially. He did note that he was concerned about some areas of the non-bank financial sector. We would be cautious about adding positions in some of the Buy Now Pay Later and digital wallet companies until we see earnings results.

- The market took a turn lower when Powell started to discuss the balance sheet. He stated that the balance sheet is “substantially” larger than it needs to be and that a “substantial shrinkage of the balance sheet” needed to be done. He did note that the economy was strong enough to stand on its own but that did little to assuage investor concern as selling pressure was already underway. Powell highlighted that the discussion is on-going. This will remain a key focus for the markets when Fed speakers start to make the rounds.

- The Housing stocks (ITB, XHB) were hit particularly hard as Powell said that the balance sheet would be primarily made up of treasuries.

- On the inflation front, it is evident that Powell & Co do not expect any assistance from the supply chain improving. Mr. Powell does not expect supply chain issues to be worked out until the second half of the year at the earliest. He sees the semiconductor issues persisting into 2023. This is important as some doves hoped that a hint of improvement around this issue would suggest a slower rate hike path by the Fed. The idea being that some of the inflation pressures would be lifted as supply met high demand.

- The Fed Chair discussed the differences between the current tightening period and how it relates to 2015. During the Q&A he stated, “We know that the economy is in a very different place than it was when we began raising rates in 2015. Specifically, the economy is now much stronger, the labor market is far stronger, inflation is running well above our 2% target, much higher than it was at that time and these differences are likely to have important implications for the appropriate pace of policy adjustments. Beyond that, we haven’t made any decisions”.

- When asked about the potential for a larger rate hike- a 50 bps push- he was rather vague but did hint that a potential two-rate hike would be on the table for discussion.

As we can see, the central bank has every intention of moving forward with its rate hike cycle.

The asset purchase will come to an end in March. The balance sheet will remain steady, but it is evident that the Fed will be looking to sell these assets into the market over the course of the next 12-24 months.

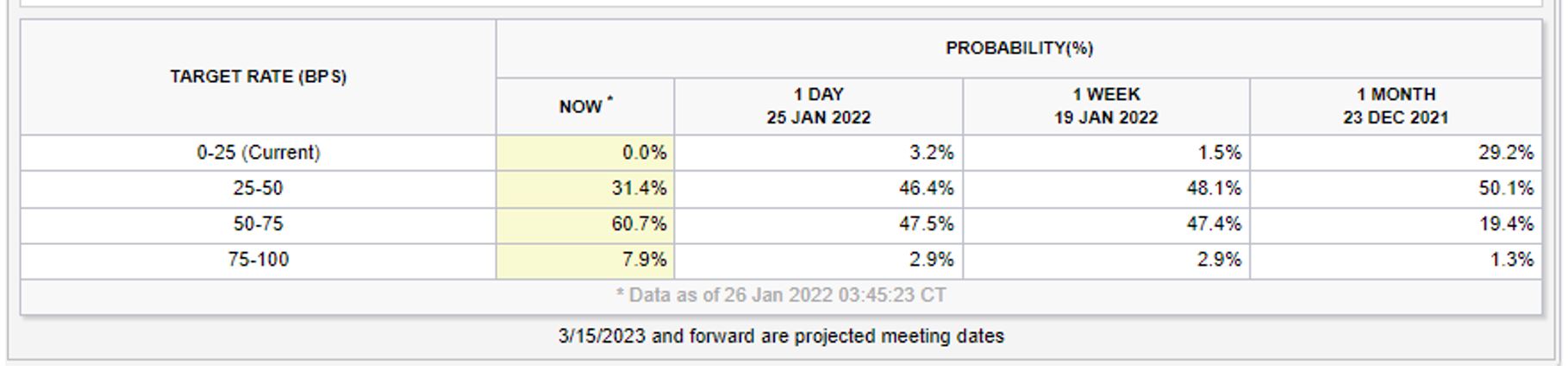

There is the potential for a 50-basis point rate hike in March. The Fed Fund Futures expectation for a two-rate hike went from 47% to 61%.

The normal cycle between Fed meetings is 1) Directive and Powell press conference; 2) Fed speakers; 3) Fed Minutes three weeks later; and 4) Beige Book two weeks ahead of the meeting.

The next phase is awaiting other Fed members commentary. Usually, they like to adjust the market’s interpretation of the Fed event to make sure everyone is on the same page. If we do not see any attempt to change the narrative around the Powell comments and reaction, then we can assume the market heard Jay Powell correctly.

The next step will be to figure out if we are getting a one or two rate hike in March and for further clarity around the balance sheet.