By Jared Higgs, Luc Cohen and Chris Prentice

NASSAU, Bahamas/NEW YORK (Reuters) – U.S. prosecutors on Tuesday accused Sam Bankman-Fried, the founder of crypto currency exchange FTX, of fraud and violating campaign finance laws and a judge in the Bahamas denied him bail, sending him to a local correctional facility instead.

The former FTX CEO, who was arrested in the Bahamas on Monday, lowered his head and hugged his parents after the magistrate judge refused bail citing a “great” risk of flight.

He was ordered remanded to a correctional facility in the island nation until Feb. 8, where he will initially held in the medical department, according to a local official.

The day’s events capped a stunning fall from grace in recent weeks for the 30-year-old, who amassed a fortune valued over $20 billion as he rode a cryptocurrency boom to build FTX into one of the world’s largest exchanges before it abruptly collapsed this year.

Bankman-Fried has previously apologized to customers and acknowledged oversight failings at FTX, but said he does not personally think he has any criminal liability.

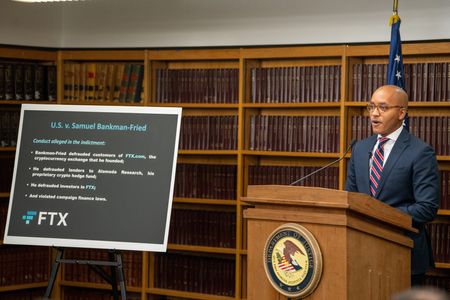

Earlier on Tuesday, U.S. Attorney Damian Williams in New York said Bankman-Fried made illegal campaign contributions to Democrats and Republicans with “stolen customer money,” saying it was part of one of the “biggest financial frauds in American history.”

“While this is our first public announcement, it will not be our last,” he said, adding Bankman-Fried “made tens of millions of dollars in campaign contributions.”

Bankman-Fried faces a maximum sentence of 115 years in prison if convicted on all eight counts, prosecutors said, though any sentence would depend on a range of factors.

Williams declined to say whether prosecutors would bring charges against other FTX executives and whether any FTX insiders were cooperating with the investigation.

In his first in-person public appearance since the cryptocurrency exchange’s collapse, Bankman-Fried appeared in court on Tuesday in the Bahamas, where FTX is based and where he was arrested at his gated community in the capital, Nassau.

He appeared relaxed when he arrived at the heavily guarded Bahamas court and told the court he could fight extradition to the United States.

Bahamian prosecutors had asked that Bankman-Fried be denied bail if he fights extradition.

“Mr. Bankman-Fried is reviewing the charges with his legal team and considering all of his legal options,” his lawyer, Mark S. Cohen, said in an earlier statement.

‘BRAZEN’ SCHEME

FTX’s current CEO, John Ray, told congressional lawmakers on Tuesday that FTX lost $8 billion of client money, saying the company showed “absolute concentration of control in the hands of a small group of grossly inexperienced, nonsophisticated individuals.”

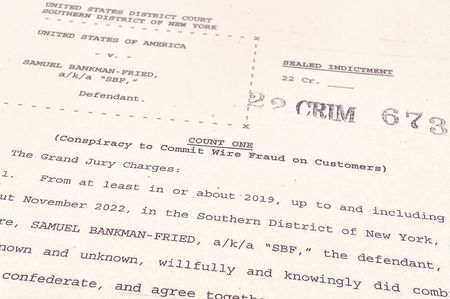

In the indictment unsealed on Tuesday morning, U.S. prosecutors said Bankman-Fried had engaged in a scheme to defraud FTX’s customers by misappropriating their deposits to pay for expenses and debts and to make investments on behalf of his crypto hedge fund, Alameda Research LLC.

He also defrauded lenders to Alameda by providing false and misleading information about the hedge fund’s condition, and sought to disguise the money he had earned from committing wire fraud, prosecutors said.

Both the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) alleged Bankman-Fried committed fraud in lawsuits filed on Tuesday.

The CFTC sued Bankman-Fried, Alameda and FTX on Tuesday, alleging fraud involving digital commodity assets.

Since at least May 2019, FTX raised more than $1.8 billion from equity investors in a years-long “brazen, multi-year scheme” in which Bankman-Fried concealed FTX was diverting customer funds to Alameda Research, the SEC alleged.

CRYPTO INVESTORS LOST BILLIONS

Bankman-Fried, who founded FTX in 2019, was an unconventional figure who sported wild hair, t-shirts and shorts on panel appearances with statesmen like former U.S. President Bill Clinton. He became one of the largest Democratic donors, contributing $5.2 million to President Joe Biden’s 2020 campaign. Forbes pegged his net worth a year ago at $26.5 billion.

FTX filed for bankruptcy on Nov. 11, leaving an estimated 1 million customers and other investors facing losses in the billions of dollars. The collapse reverberated across the crypto world and sent bitcoin and other digital assets plummeting.

The collapse was one of a series of bankruptcies in the crypto industry this year as digital asset markets tumbled from 2021 peaks. A crypto exchange is a platform on which investors can trade digital tokens such as bitcoin.

As legal challenges mount, the U.S. Congress is also looking at crafting legislation to rein in a loosely-regulated industry.

FTX has shared findings with the SEC and U.S. prosecutors, and is investigating whether Bankman-Fried’s parents were involved in the operation.

The attorney general’s office of the Bahamas said it expected Bankman-Fried to be extradited to the United States.

Bankman-Fried resigned as FTX’s CEO the same day as the bankruptcy filing. FTX’s liquidity crunch came after he secretly used $10 billion in customer funds to support his proprietary trading firm Alameda, Reuters has reported. At least $1 billion in customer funds had vanished.

(This story has been refiled with a corrected picture caption)

(Additional reporting by Luc Cohen and Jack Queen in New York and Hannah Lang, Chris Prentice and Susan Heavey in Washington; Writing by Nick Zieminski and Deepa Babington; Editing by Noeleen Walder, Megan Davies, Anna Driver and Matthew Lewis)