May 28, 2026

Broadcom’s $73B Backlog

Custom silicon, a $73B backlog, and Q2 earnings on June 3

Editor’s Note: Louis Navellier has spent 40+ years identifying stocks before major tech waves – his system helped him flag Nvidia before its 82,000% run. Today, he’s revealing the three stocks at the center of the biggest AI buildout in history. Click here for the full story or read more below.

Dear Reader,

Goldman Sachs just predicted 300 million jobs will disappear.

Not in 10 years. Not in 5.

This is starting NOW.

30,000 layoffs at UPS. 16,000 at Amazon. Factories are going “lights out” with zero human workers.

And now Elon Musk’s “Project Apex” is set to accelerate this labor crisis.

A Nobel Prize-winning scientist says what Elon is building “could have an even greater impact on society than the internet.”

Nvidia’s CEO calls it “superhuman.”

And competitors are so panicked, they’re flying spy planes over the facility to figure out how it works.

See what Elon is really building – and the stock at the center of it all.

Look, I’m not telling you this to scare you…

I’ve spent 40+ years analyzing technological shifts like this. My proprietary system has helped me identify winning stocks before every major tech wave.

I’m telling you because on the OTHER side of this disruption is a historic investment opportunity.

The last time a technology shift this big happened, early investors in the right supply-chain stocks had the chance to see extraordinary gains. Lithium Americas: 1,452%. NIO: 1,755%. Blink Charging: 3,648%. All in under two years.

I’ve pinpointed one tiny company at the center of Elon’s AI revolution – 49 times smaller than Tesla – that’s become the “secret weapon” of Microsoft, Meta, Amazon, and Google. I’ll also share two more stocks positioned for this wave – but I believe this one is the must-own.

Click here for the full story in this free briefing, including the name and ticker of my #1 pick.

Regards,

Louis Navellier

Senior Investment Analyst, InvestorPlace

P.S. My #1 AI pick is 49 times smaller than Tesla but it’s powering Microsoft, Meta, Amazon, and Google. Get the name and ticker in this free briefing before this story goes mainstream.

FEATURED

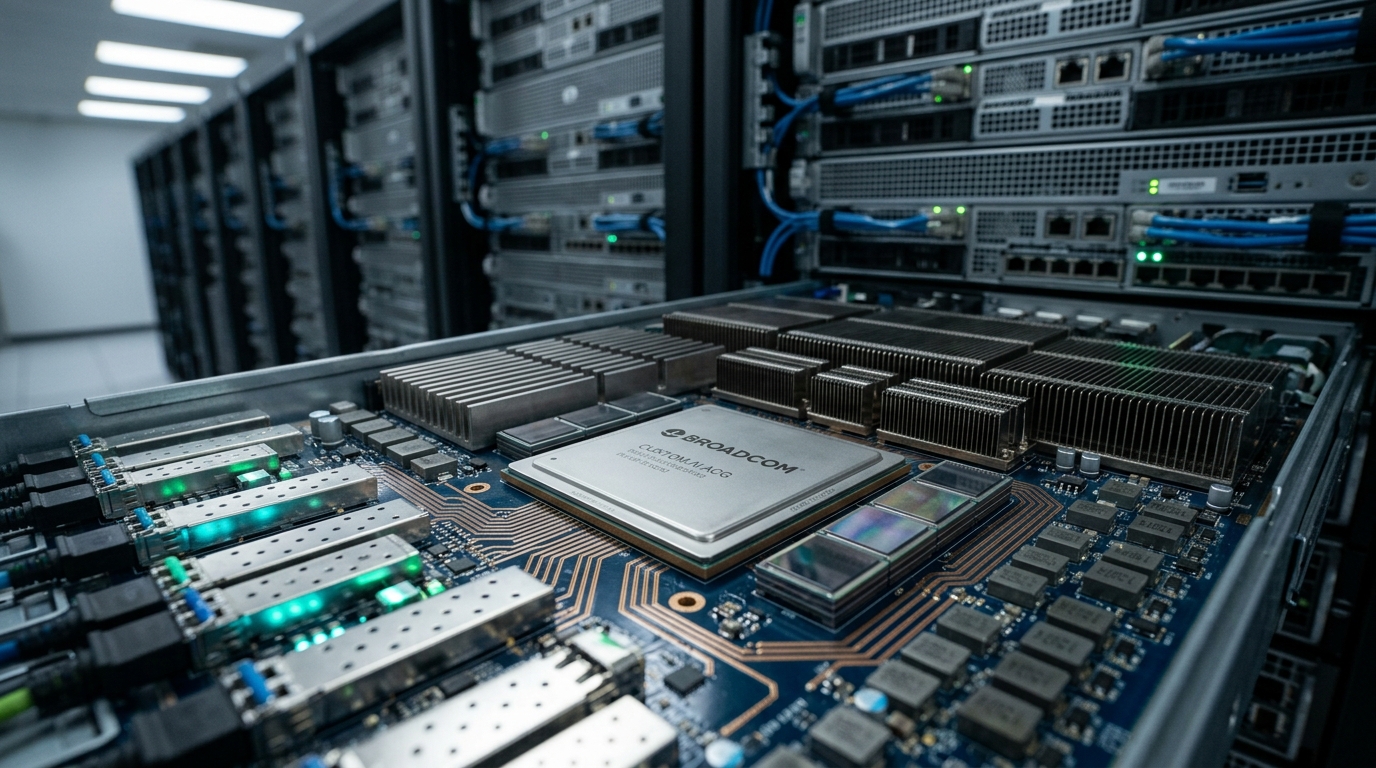

Broadcom’s $73B Backlog

Everyone talks about Nvidia. Fair enough. But while one name absorbs all the oxygen, Broadcom has been running a quieter, arguably more durable operation. Q1 fiscal 2026: record revenue of $19.3 billion, up 29% year-over-year. AI semiconductor revenue came in at $8.4 billion, up 106% year-over-year, ahead of Broadcom’s own internal forecast. That last part matters more than the headline number. When a company outpaces its own guidance by that margin, you pay attention. CEO Hock Tan then guided Q2 AI chip revenue to $10.7 billion, with total quarterly revenue expected at $22 billion, a 47% year-over-year jump that blew past the analyst consensus sitting around $20.4 billion. Q2 results drop June 3 after market close.

Here’s the thing about Broadcom’s actual business. It’s not a single product, not a single customer. Google’s Tensor Processing Units run on Broadcom-designed silicon, and HSBC estimates TPU-related shipments account for roughly 78% of Broadcom’s ASIC revenue today. Meta’s first gigawatt of Broadcom-designed compute is expected to deploy in 2027, a contract Broadcom has framed as a $12 to $15 billion revenue opportunity. OpenAI’s first-generation XPU also goes into volume production in 2027 at over one gigawatt of capacity. Each new customer represents three to five years of recurring silicon revenue. That’s the structural point most people skip.

Slight tangent, but it matters: Broadcom also just launched the BCM68850, the industry’s first 50G home gateway chip with integrated AI acceleration. Most investors aren’t following the edge AI product line. They probably should be.

On valuation, the stock is trading around $422 as of late May, up roughly 22% year-to-date and about 125% over the past twelve months. Hock Tan has stated Broadcom has “line of sight” to $100 billion in AI chip revenue by 2027. The company also carries a $73 billion AI-specific order backlog.

What’s interesting is the risk hiding in plain sight. The software segment, built around VMware, grew just 1% last quarter. Trade policy and export controls remain a real overhang on the sector. And semiconductor cycles have a way of humbling even the best guidance.

June 3 is close. Worth a closer look before then.